Building a 50-Year Financial Plan for a Sorority House

Reserve studies, renovation cycles, inflation assumptions, and the leadership succession problem no one wants to talk about.

Most sorority house corporations plan in four-year cycles — anchored to the academic calendar, driven by whoever happens to be treasurer that year. It’s an understandable approach. Leadership turns over constantly, and a functioning HVAC system feels like a long-term win. But a sorority house is not a dorm room. It is a capital asset worth millions of dollars, home to dozens of women, and expected to operate continuously for generations.

What follows is a practitioner’s framework for thinking about your chapter’s financial health across a 50-year horizon. We cover the mechanics of reserve studies, how renovation cycles compound on each other, how to build conservative investment return assumptions into your reserve fund, and — critically — how to design financial systems that survive leadership turnover.

“The chapter that built the kitchen in 1998 is not the chapter that will replace it in 2033. Your financial plan has to outlast every treasurer you’ll ever elect.”

Why 50 years? The compounding case for long-horizon thinking

A 50-year plan sounds unwieldy. No single leadership team will see it through. But the purpose of a long-horizon plan is not to predict the future — it is to force an honest accounting of the assets you’re stewarding and the obligations that come with them.

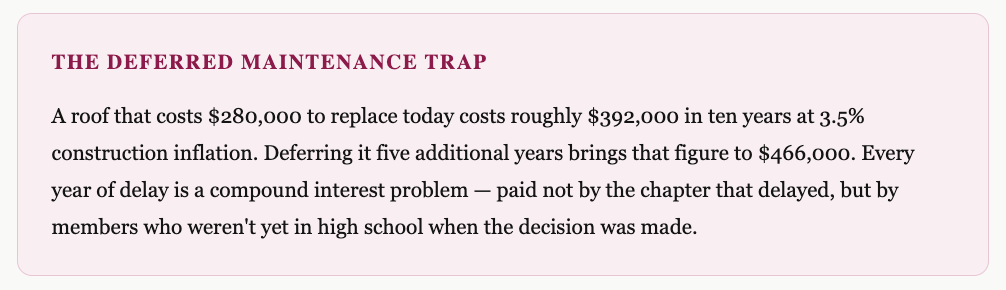

Consider a typical sorority house built in the 1960s or 1970s. Major building systems — roof, HVAC, plumbing, electrical, exterior — each carry useful lives of 20 to 30 years. In a 50-year window, every system will need replacement at least once, and some will cycle twice. Fail to plan for those replacement events and you are, in effect, borrowing from future members to subsidize current operations — lowering dues today by deferring maintenance that someone else will pay for later, at a much higher inflation-adjusted cost.

Reserve studies: the foundation of everything

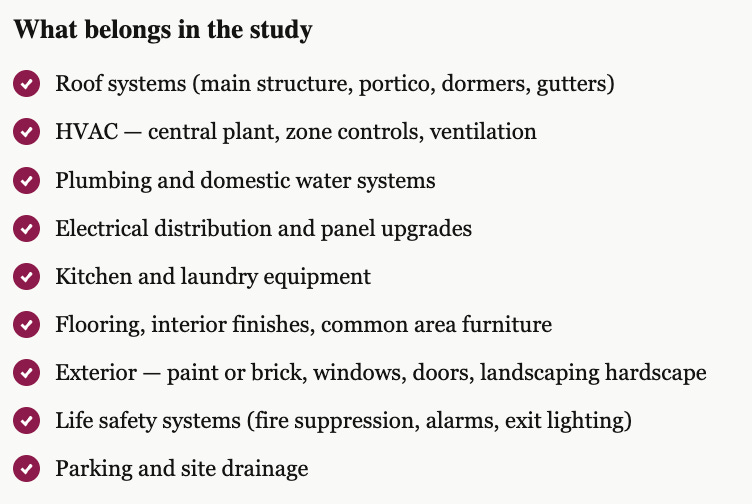

A reserve study is a professional assessment of your building’s major components, their remaining useful lives, and the cost to replace them — discounted and scheduled across a multi-decade horizon. Think of it as a capital budget stress test for your physical plant.

A well-executed reserve study does three things: it inventories every major component with a replacement cost and an expected service life; it produces a funding schedule showing how much should be set aside each year to meet future obligations; and it calculates a “percent funded” metric — the ratio of your current reserve balance to the theoretically ideal reserve balance.

Reserve studies should be updated every three to five years, with at least one on-site inspection. The study produces both a threshold (minimum) funding schedule and a full (ideal) funding schedule. Aim for the full schedule. Chapters that operate near threshold funding are perpetually one bad winter away from a special assessment.

Renovation cycles: how systems pile up

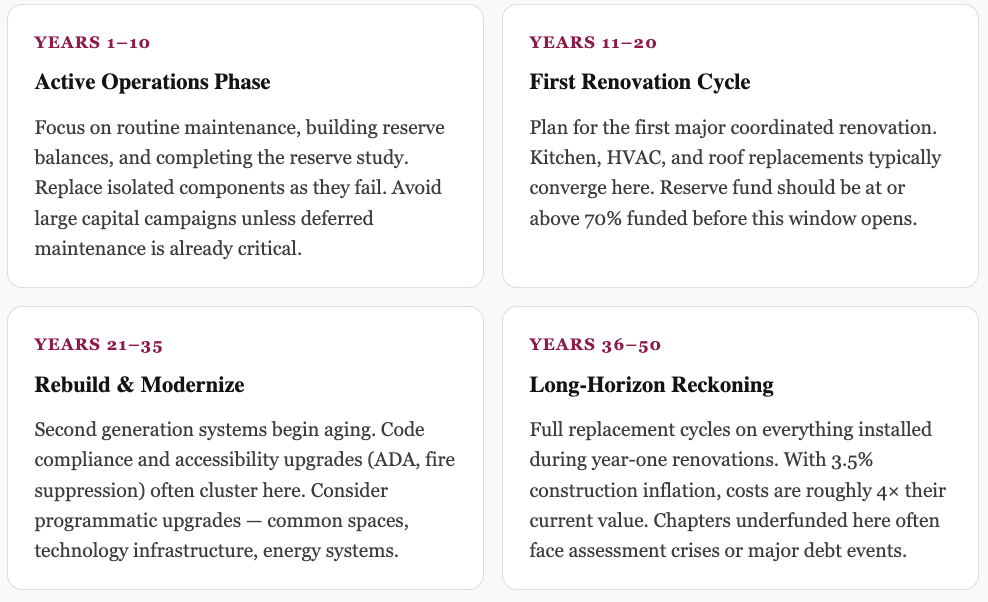

One of the most common planning errors is treating major renovations as isolated events. In reality, building systems age in clusters. A chapter house built in 1975 that got a major renovation in 2005 is likely entering a second synchronized replacement window right now: roofs installed in 2004 are hitting their 20-year mark; HVAC systems from the same renovation are approaching end-of-life; the commercial kitchen is operating on borrowed time.

The practical implication: when planning a major renovation, do not replace only what is broken. Replace everything within two to four years of end-of-life at the same time. Mobilization costs — contractor setup, design fees, permitting, disruption to operations — are largely fixed. Combining a roof replacement with an HVAC upgrade in a single project often saves 15 to 25% over doing them separately.

Inflation assumptions: construction costs don’t move like the CPI

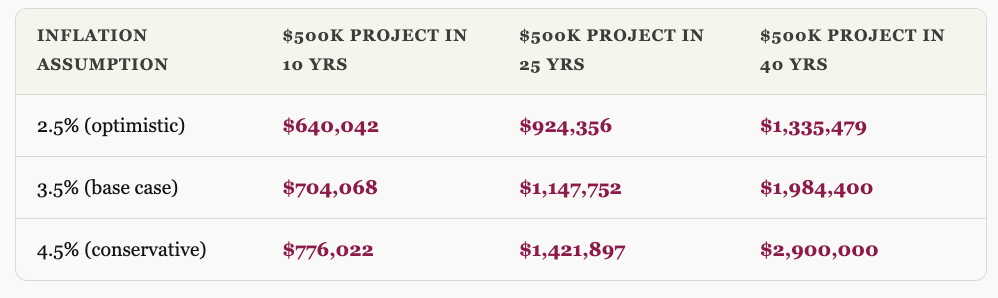

General consumer price inflation is a poor proxy for construction cost planning. Building material costs, skilled labor rates, and commercial contractor margins each follow their own supply dynamics. Construction cost indexes — ENR’s Construction Cost Index is widely used — have averaged 3 to 4.5% annual increases over long periods, with periodic spikes (the 2021–2023 period saw 10%+ in a single year) and occasional flat or negative years.

Our recommendation: build your long-range capital plan using a 3.5% construction inflation rate as the base case, run a sensitivity check at 4.5%, and never plan below 2.5% regardless of current economic conditions. The downside of over-funding is a healthy reserve. The downside of under-funding is a $400,000 special assessment that destroys recruitment.

“Don’t plan your roof replacement using the same inflation assumption you’d use for grocery budgets. Construction costs have their own math.”

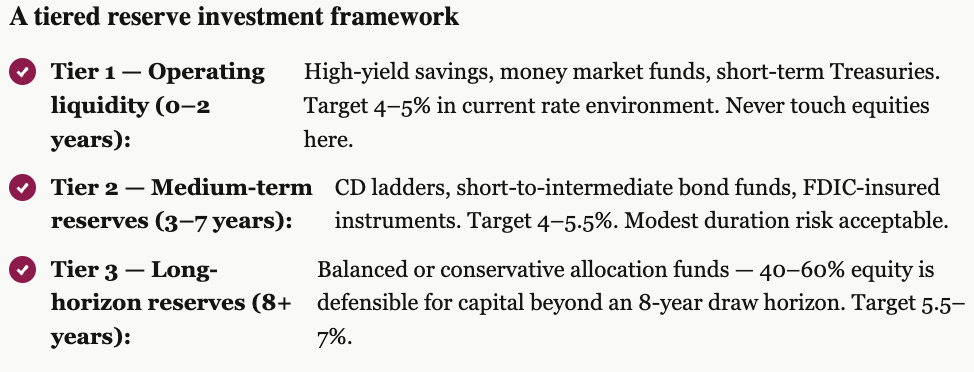

Investment return assumptions: what your reserve fund can realistically earn

Reserve funds are not endowments. They are operating capital with known future draws. This matters enormously for how you invest them.

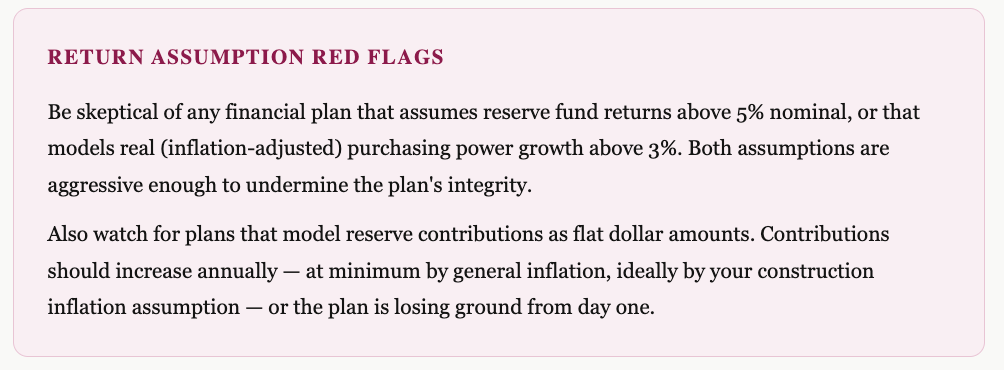

The temptation for boards sitting on a $400,000 reserve is to reach for equity returns — the stock market averaged 10% per year, after all. But a reserve fund that loses 30% in a market downturn right before a major renovation needs to either defer that renovation or levy a special assessment. Neither is acceptable. Reserve funds need to be managed for capital preservation and liquidity, not return maximization.

For modeling purposes, use a blended after-inflation return assumption of 2 to 3% — meaning your nominal return assumption minus your construction inflation assumption. If you're earning 5% nominally and planning against 3.5% construction inflation, your real purchasing power growth is roughly 1.5%. Models that assume 6–7% real returns on reserve funds are fantasy; the plans they produce will fail.

Succession planning: the problem no one talks about

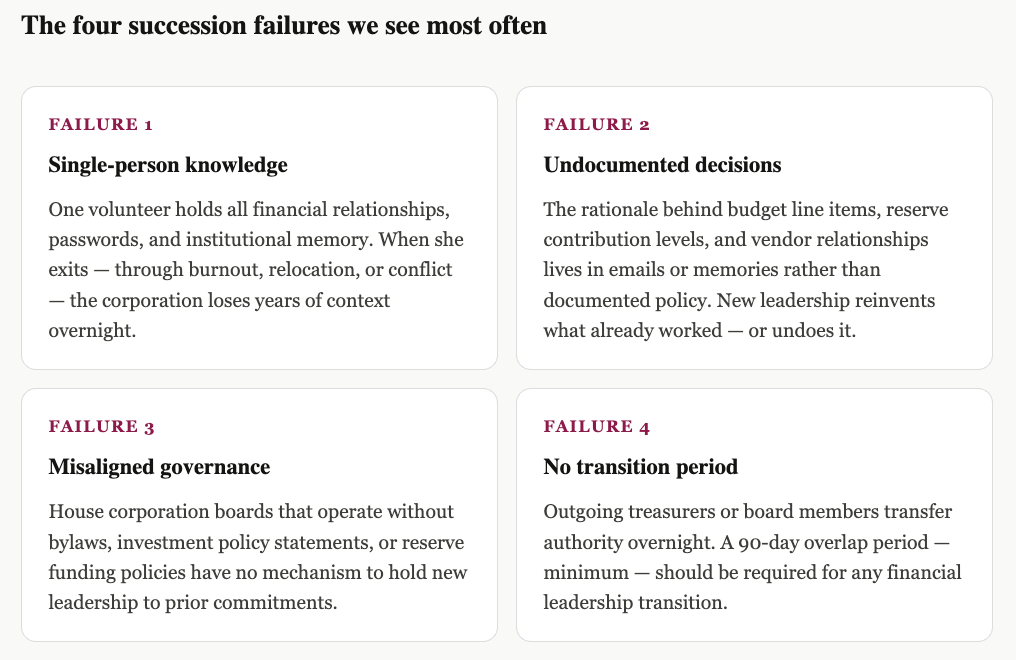

Every piece of financial infrastructure we’ve described above depends on institutional continuity. The reserve study means nothing if the new treasurer doesn’t know it exists. The investment policy expires in practice the moment someone moves the reserve fund into a personal brokerage account “to get better returns.” The 50-year capital plan is worthless if it lives only in one alumna’s spreadsheet.

Financial succession is not a governance nicety. For a house corporation managing a multi-million dollar asset, it is an existential risk management issue.

Building a succession-proof financial system

Adopt a written Investment Policy Statement (IPS) governing reserve fund allocation, permissible instruments, and rebalancing triggers. Board-approved; cannot be altered unilaterally.

Maintain a Reserve Funding Policy specifying the minimum annual contribution and the target funded percentage. Make it a covenant in your house corporation bylaws.

Store all financial documents — reserve studies, audits, vendor contracts, the capital plan itself — in a shared, board-accessible cloud repository, not on personal devices.

Require dual signatories on all reserve fund disbursements above a defined threshold (suggest $2,500).

Engage a CPA to produce reviewed (not merely compiled) financial statements annually. Reviewed statements create a paper trail that survives personnel transitions.

Brief incoming board members with a structured financial onboarding — at minimum: the reserve study, the capital plan, the IPS, and the current bank and investment account summary.

Consider a professional property management or financial management firm as a permanent institutional anchor — one party whose knowledge doesn’t cycle out every four years.

Putting it together: the 50-year plan in practice

A 50-year plan does not need to be a 200-page document. The most effective versions are living spreadsheets — updated annually by whoever holds the treasurer or executive director role — built on five components:

1A component inventory with replacement cost and remaining useful life, sourced from your most recent reserve study

2A 50-year cash flow model — contributions in, construction draws out — using your chosen inflation and return assumptions

3A funded percentage tracker updated each year after the annual audit

4A renovation sequencing calendar showing anticipated major project windows and estimated costs in future dollars

5A scenario analysis tab that stress-tests the plan at higher inflation and lower investment returns

Review this model annually with the full board. Present the funded percentage trend — not just the account balance. A rising balance hiding a declining funded percentage is a warning sign, not a success story.

The goal is not to predict 2076. The goal is to make sure the chapter in 2076 is not paying for decisions — or non-decisions — made today. That is what stewardship means across generations.

Get the 50-Year Capital Plan Template

Sorority Support members can download our 50-year capital planning spreadsheet, reserve study checklist, and Investment Policy Statement template — built specifically for house corporations.